NEP 2025: A policy win for the green hydrogen industry?

In Indonesia’s new Government Regulation No. 40/2025 on the National Energy Policy (NEP 2025), one line could shape the country’s energy future: hydrogen and ammonia “shall preferably be produced from renewable energy sources to generate green hydrogen.”

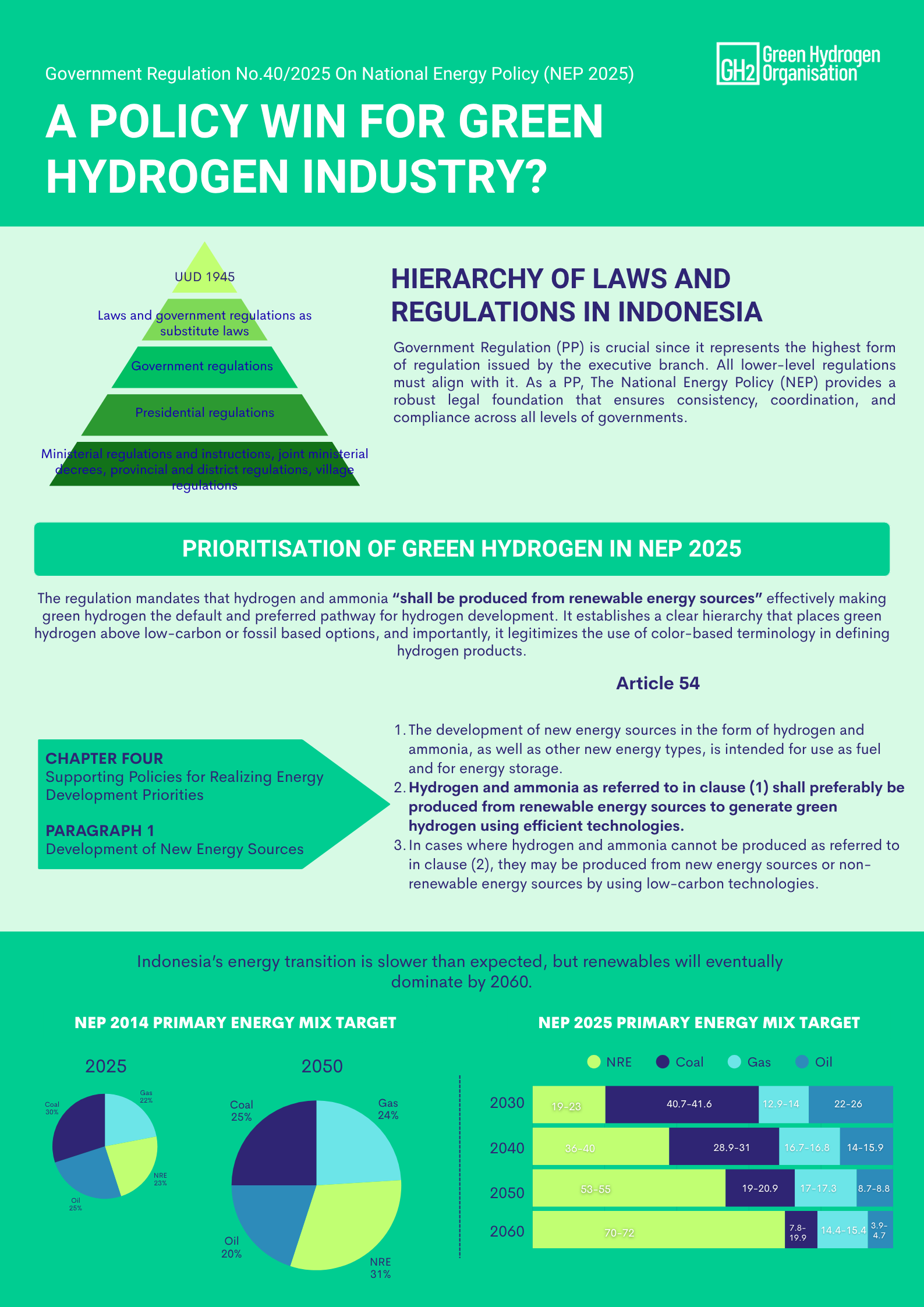

This single phrase makes green hydrogen the default and preferred pathway for the nation’s hydrogen development. It elevates hydrogen made from solar, geothermal or hydropower above fossil-based alternatives. For the first time, the government officially recognizes color-based hydrogen terminology, a small but powerful signal of where policy priorities now lie.

What appears in a Government Regulation (Peraturan Pemerintah or PP) carries weight. A PP represents the highest form of regulation issued by the executive branch and all lower-level regulations must align with it. As such, NEP 2025 provides a strong legal foundation that ensures consistency and compliance across all levels of government.

The hydrogen section of NEP 2025 stands out: hydrogen and ammonia are now written into nearly every corner of the energy system from electricity generation to transport, industry, and even household use.

Implementation Challenges

Yet, the path ahead will not be simple. While green hydrogen is given top priority, the regulation still permits fossil-based hydrogen where renewable production is not yet feasible. That flexibility may be pragmatic, but it also risks locking the country into costly carbon-capture projects that prolong fossil dependency.

Additionally, the broader policy picture is mixed. Indonesia’s long-standing target of achieving 23 percent renewable energy by 2025 has now been pushed back to 2030. Coal remains deeply entrenched, projected to supply more than 40 percent of electricity through 2030 before gradually declining to around 8–20 percent by 2060. By then, renewables are expected to account for about 70% of the power mix while the remaining 129 million tons of CO₂ emissions will be offset through forestry and land-use absorption.

The policy’s endorsement of hydrogen or ammonia co-firing in coal power plants sends another mixed signal. It positions hydrogen not as a clean substitute but as a supplementary fuel that extends coal’s lifespan. In an era when renewable and battery costs are falling rapidly, Indonesia must be careful not to lock its future to yesterday’s technologies.

The road ahead therefore looks uneven. The delay of the renewable target to 2030, continued reliance on coal, and growing role for biofuels raise hard questions about where the clean electricity for hydrogen will come from. Several NGOs have voiced concern that biofuels could divert resources from more sustainable renewables, undermining Indonesia’s green ambitions. It is critical that Indonesia adopts a robust Low-Carbon Hydrogen Standard, one that we have actively supported and helped to develop.

Next Steps for Indonesia

In a nutshell, NEP 2025 marks a turning point that should finally end the long-running blue versus green hydrogen debate in Indonesia. For the first time, a top-level energy policy explicitly states that hydrogen and ammonia should preferably be produced from renewable energy.

This clarity matters. It positions green hydrogen as the norm, not a side option. As Southeast Asian countries racing to both decarbonise domestic industries and pursue export opportunities, NEP 2025 gives Indonesia firmer footing and offers developers with regulatory certainty needed for long-term planning.

Over the past year, we have observed shifting priorities within Indonesia’s energy leadership following the appointment of a new energy minister in 2024. The change has brought a noticeable dip in political attention toward climate and hydrogen, prompting us to adapt our approach and build broader coalitions. At the same time, the release of NEP 2025 came as an encouraging shift especially to many in industry who had grown skeptical about the government’s commitment to green energy transition.

Still, regulations alone won’t deliver results. A true victory for green hydrogen will not come from legal language, but from economics. Renewable power and electrolyzer costs must fall low enough to make green hydrogen competitive with fossil-based alternatives. That will require accelerating renewable deployment, lowering power costs, sustaining public investment, and encouraging private risk-taking, all while phasing out fossil fallback options.

NEP 2025 gives green hydrogen a policy win but the scoreboard will depend on how fast renewables expand and costs decline.

The regulation gets the vision right. It places renewable power and green hydrogen at the center of the national energy future. But vision alone won’t bend the cost curve. The next chapter will be written not in policy papers, but in power plants, grids, and investments that make green hydrogen truly competitive.

Rifan Bachtiar

Country Manager, Indonesia

GH2